Presentation Paper

Introduction

When discussing the future of global agriculture, it is always tempting to trot out the United Nations forecast of a “70% increase in global food demand by 2050”.

This forecast paints a pretty positive picture, from a farmers’ perspective. After half a century of declining real prices for agricultural commodities, it suggests we have entered a phase of improved profitability for the farm sector.

However, those of you who keep a close eye on global agricultural commodity markets will be well aware that the greatest challenge for Australian farmers over recent decades, and even at present, is low prices associated with the over-supply of key agricultural commodities.

We have seen it in particular in dairy, sugar and wine over recent years, and were it not for the drought in eastern Australia, the same would apply to grains. Despite increasing global demand, it seems that real international prices for many globally traded agricultural commodities generally continue to decline.

For the farming sector in a nation such as Australia which has some of the lowest agricultural trade barriers and farm subsidies in the world, this should mean that the only way to enhance the economic value of agriculture is to increase the volume of farm output.

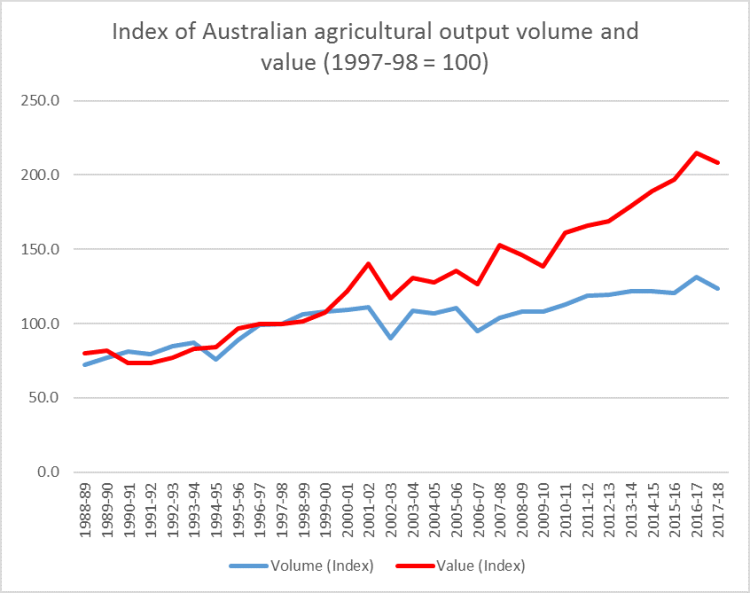

A close look at available statistics indicates this has occurred over the last 30 years, with the volume of annual agricultural output increasing by about 25 per cent over this period.

But surprisingly, the annual value of Australian agricultural output has increased by 105 per cent over this same period and, even when adjusted for inflation, the growth in value outstrips the growth in volume.

What these figures highlight is that there has been a major shift in the agriculture sector in Australia over the last two decades. And it is a shift that has far-reaching consequences for all involved in its future.

I will explore some of the implications of this shift in my talk today, discuss the work we’re doing at the Australian Competition and Consumer Commission (ACCC), and close with my thoughts about what needs to be done to enhance future opportunities to increase the value of Australian agriculture.

Current state of the market

Producing enough food to meet the projected 70 per cent growth in global demand by 2050 may sound challenging, but when the figures are closely analysed, achieving that target is actually quite viable.

It equates to a target of 1.3 per cent growth in annual global food output, which is well below current levels of 2.2 per cent pa.

And while it is often claimed that this level of output growth cannot be sustained due to limits on available resources such as land and water, it is notable that most of the output growth over the past two decades was due to productivity gains, rather than an expansion in the amount of land and water used for agriculture.

In fact, in many developed nations, including Australia, the amount of land and water used for agriculture has declined significantly while output growth has persisted.

A key factor in the growth of global agricultural output over recent years has been the continuing development of the agricultural sectors of Eastern Europe, South America and Asia.

Farmers in these regions are now highly competitive in global agricultural commodity markets. This is due to factors such as low costs, abundant natural resources and rapidly improving productivity.

This means that, despite the positive future demand growth projections, there has generally been a continuation of the long-term trend of declining real commodity prices, interrupted only occasionally when seasons or trade disruptions intervene.

Recognising these global trends, it would be expected that Australian farmers would be experiencing low profitability, given our relatively high costs.

There is some evidence of this in sectors such as dairy and sugar, but the general picture for agricultural commodity prices received by farmers in Australia is actually quite positive, as the graph I showed earlier highlights.

This is because Australian farmers and processors have increasingly altered their production and processing systems to target higher value or premium markets, rather than just continuing to attempt to compete on a least-cost basis.

This change is very evident in the livestock sectors; the beef industry, for example, is transitioning from mince beef to Wagyu exports. The same can, however, be said for the horticulture, cotton and wool sectors; and to a lesser extent, grains and oilseed.

And more generally, Australia has managed to retain and even enhance its reputation as a reliable supplier of high quality and safe agricultural produce, meaning that even in generic commodity markets, there is often an “Australian” premium.

Increasing consumer demand for premium produce

Due to the change from a volume to a value focus, the Australian agriculture sector in general is now servicing markets in which relatively wealthy consumers are spending a decreasing proportion of their disposable income on food, and they therefore can afford to be quite selective about which food they purchase.

They are no longer content to purchase whatever is available, and are becoming more and more selective. They want quality, safety, integrity, and they want to know about the production systems and input use that comes with the food they purchase.

This applies even in the live cattle export market, which is servicing increasingly wealthy consumers in nations such as Indonesia, Vietnam and China.

Wealthier consumers tend to be more aware of, and prepared to act on issues such as the environment, animal and worker welfare, and reflect these preferences in their purchases.

In response, retailers and processors are taking action to ensure their ‘brand’ and the products on their shelves meet the perceived needs of premium consumers.

Some are doing so by transferring additional product and compliance requirements on to their producer-suppliers.

At the same time, producers are also responding to the opportunities created by premium markets. They are choosing to change production and management practices to improve quality and safety, and they are choosing to meet provenance, credence, integrity and traceability requirements.

An obvious example here in the Northern Territory is OBE organic beef.

However, many of the product characteristics consumers are prepared to pay a premium for cannot be determined just by looking at the product.

For example, an organic rump steak usually looks the same as a conventional rump steak. Wool from unmulesed sheep looks the same as wool from mulesed sheep. And Australian baby formula looks no different to baby formula from another nation, once out of the can.

This means that critical to continuing success in these premium markets, and indeed the “Australian premium”, is the level of trust consumers have in the information they are given about the available products, and the national systems that underpin them.

Consequently, producers, exporters and processors no longer just send livestock or produce on a truck or in a container. They now send those animals or products together with a package of information.

For a producer, that information might be a vendor declaration, or an animal health statement, or details of organic or environmental accreditation, or information in compliance with exporter, processor or retailer standards.

For a processor or exporter that information will invariably include details of compliance with relevant safety and other standards, as well as confirmation of its Australian origin.

In some cases, that package of information more than doubles the value of the product. For example, a major retailer currently sells cage eggs for $3.00 dozen, and free-range organic eggs for $8 per dozen.

Given that most people cannot visually distinguish between cage eggs and organic free-range eggs, the consumer trust in the ‘information package’ associated with the organic free-range eggs is worth $5 dozen – more than the full value of the cage eggs.

There are two major implications of this change.

The first is that the integrity of the ‘information package’ associated with agricultural products is rapidly increasing in importance, and there is a need for all involved in the sector to ponder whether current systems are robust enough to sustain that integrity.

The second implication is that market transparency is decreasing. This is occurring because processors and exporters are increasingly dealing directly with producers to better manage a consistent supply of higher value products, and bypassing the more traditional agricultural markets and the public price discovery systems associated with those.

In doing so they are also using more and more complex pricing systems that target very specific product qualities and characteristics. The prime cattle pricing grids being published by major beef processors, or the pricing formulas being used by dairy processors are examples of this.

While many producers are benefitting from their direct dealings with processors and exporters, market transparency is decreasing which mean that producers cannot easily compare offers or understand changes in supply and demand, and are therefore in a weakened bargaining position in their price negotiations.

This issue is less immediately relevant to the live export market, although the lack of price transparency and objective market reporting that is a feature of this market also leaves cattle producers in a weaker bargaining position.

The ACCC has responsibilities under Australian law to promote competition in markets, and product integrity and market transparency are both issues that impact on competition.

I believe there is a need for some careful consideration of policy decisions in relation to these two issues, in order to ensure Australian agriculture can continue to grow in value.

Maintaining consumer trust in product claims

The ACCC has several areas of responsibility that have an impact on the level of trust that consumers have in the information they are provided about the foods they purchase.

One of our roles is to enforce the laws which make it an offence to engage in misleading and deceptive conduct, in making claims about products.

As I highlighted in the earlier reference to the price difference between cage and free-range eggs, the trust that consumers have in the product information they are provided is absolutely critical to their perception of the value of that product.

Consider, for example, the implications if OBE Organic experienced a loss of consumer confidence in the integrity of organic claims made about their beef. The financial implications of any loss of consumer trust in the integrity of that product would be very large.

A core responsibility of the ACCC is to ‘police’ the integrity of claims by producers and processors, and to take action when there is evidence that claims are ‘misleading and deceptive’.

The ACCC has taken legal action in the past against egg and beef producers who were making misleading claims, with our most recent example resulting in a fine of $750,000 for a Western Australian egg producer falsely making ‘free-range’ claims.

However, allegations of false claims about organic status can be quite difficult to take action on, as even very detailed analytical testing may not provide conclusive proof, and there are a multiplicity of different organic standards in Australia.

It is also the case that a farm business does not need to have organic certification in order to be able to claim its domestically-marketed products are organic.

A similar situation applies in relation to claims made about farming management systems (for example pasture fed or grain fed), and to claims about product origins (for example Queensland beef).

These issues are complicated by the fact that even when sectors (such as the red meat industry) have agreed on the definition and standards associated with the use of particular terms, (such as are contained in the AUS-Meat language standard), there is nothing to prevent the use of these terms in domestic markets for products that have not been produced strictly according to those standards, unless the use of those descriptors could be considered misleading.

To illustrate this point, while the beef industry has developed a minimum standard for ‘pasture-fed’ claims under the Pasturefed Cattle Accreditation System (PCAS), it would be difficult to prosecute someone for misleading and deceptive conduct who used the term pasture-fed to describe beef from cattle that were substantially fed on pasture, but did not strictly comply with the PCAS.

In response to concerns about the misuse of free-range claims for eggs, the relevant state and federal ministers agreed on a National Information Standard, which was adopted and came into effect in April 2018.

This standard details certain minimum requirements for those wishing to claim that their eggs are free range. Associated with this information standard, a ‘safe harbour’ defence has been introduced into the Australian Consumer Law, which means that if an egg producer can demonstrate compliance with the standard, they are legally protected from allegations of misleading and deceptive conduct.

I think there is some merit in beef industry considering this approach. If the AUS-Meat language standard was given similar legal recognition under Australian Consumer Law it would better protect the credibility of industry-agreed standards in domestic markets, and at the same time reduce consumer confusion.

Market transparency

As I noted earlier, a second issue that emerges as a consequence of the change towards premium markets, is more complex and less transparent pricing systems, and reduced market transparency.

This often results in a transfer of extra risk to farmers, and also makes it more difficult for farmers to compare prices they are being offered.

This obviously has the potential to reduce competition between processors and exporters, especially in situations where there are only two or three competing in a market.

This problem has emerged in relatively concentrated agricultural markets, such as beef and dairy, where pricing grids typically incorporate a large number of premium and discount factors, which make a headline price almost meaningless.

While beef cattle saleyard prices do add to market transparency, as more and more cattle are consigned directly to processors or exporters, the relevance of saleyard indicator prices declines.

Reduced market transparency has the effect of lessening competition in markets, and partly arises because dominant firms can make more profits by ‘sharing the market’, rather than competing fiercely on price for every consumer or producer.

Processors and exporters have much better information about supply and demand conditions in markets, which means that producers are always at a disadvantage in negotiating prices. This imbalance is made worse when pricing systems are complex and non-transparent.

Developing good policy responses to this problem is a real challenge. There is no doubt that direct supply arrangements between producers and processors can result in improved supply chain efficiencies, from which both can benefit.

However, this will generally only occur when processors and producers have relatively equal bargaining power.

Given that processors require scale to compete globally, there will inevitably be a large imbalance in bargaining power. However, a number of different policy responses have been adopted internationally to address this imbalance, while retaining industry competitiveness. These include:

- mandatory public price reporting (in the US beef sector);

- detailed price monitoring and reporting by government (as occurs in the EU)

- reference pricing (involving the development of one or a number of ‘model’ supplier profiles, which are used to calculate and compare prices offered by competing processors); and

- default prices, which processors in a market are required to publish and make available to all their suppliers as a starting point for price negotiations;

All of these have advantages and disadvantages, which vary depending on the market in question

The ACCC, through its agriculture unit, has been heavily involved in investigations and analysis to better understand these changes, and to assist in the development of appropriate policy responses.

Our beef and cattle market inquiry identified reduced market transparency as a growing threat to competition in Australian cattle markets, and we made recommendations to try and address this.

A number of these have been adopted by industry or are under consideration by government. These include

- broadening the scope of market reporting by MLA,

- having processors simplify their pricing grids and make them more readily available,

- having commission buyers disclose who they are buying for at saleyards,

- introducing objective carcase measurement, and

- standardising the national licensing of livestock agents.

While some of these have been acted on, further progress to improve competition in the sector will require strong support from cattle producers.

Conclusion

In concluding, it is important to be aware that the agriculture sector in Australia is undergoing significant change as the sector moves to higher-value markets and adjusts to the increasing specificity of consumer requirements.

The changes that are occurring are generally beneficial, and demonstrate that the sector is responding to market signals in ways that allow it to grow in value, despite resource constraints.

However, the changes that are occurring have increased the importance of, and value associated with product integrity, and at the same time increased the potential harm the sector will experience if consumer trust is damaged. This makes it very important that we ensure the systems and policies in place that create consumer trust are robust and reliable.

At the same time, reduced market transparency creates an increased risk that the benefits of the greater value generated will not be shared through the entire value chain. Finding ways to address this issue without reducing the international competitiveness of the entire sector is a growing challenge.

There is no doubt that there is much work to be done. I look forward to continuing our work together to ensure we have a competitive and world-class agriculture sector.

Thank you.